When you’ve decided to make real estate your career, it’s not a good idea to just wing it. Winging it will not lead you to success. Winging it may certainly lead you down a path of confusion, wasted money, and unnecessary mistakes.

Plans serve a purpose. Having a plan doesn't mean you have to be rigid. You can be flexible within the plan as long as you keep your eyes focused on the end goal.

Why Agents Need a Real Estate Business Plan

A real estate business plan is an integral tool for any real estate agent looking to increase your success. Depending on the goals of your business, a plan can be tailored to reflect areas such as market trends, competition, lead generation strategies, and marketing approaches. By providing focus and tending to opportunities in each of these areas, you can maximize success potential and get your business where you want it to be.

Success stories abound showing the benefits of having a well-crafted real estate plan. A good real estate business plan will help you assess where your current efforts are bringing you and provide guidance as to what changes need to be made in order to hit your long-term goals.

This could include an analyzed assessment of current bidding patterns or advice on running effective open houses and networking events. Investing time into creating a thorough business plan will give you valuable insight into the best way to navigate emerging markets and develop new growth strategies for your endeavor.

Create Your Real Estate Business Plan

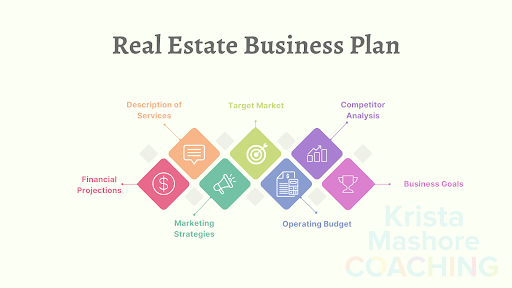

A real estate business plan is the foundation of any successful venture in this field. It serves as a roadmap by outlining goals and objectives, as well as how to achieve them. It also clarifies expectations and identifies areas of opportunity. The plan should be comprehensive, detailing every aspect of the business, from operational costs to marketing strategies.

When crafting a real estate business plan, it’s essential to consider the following:

- A description of the services provided

- The target market

- Competitor analysis

- Financial projections

- Marketing strategies

- An operating budget

- Business goals

It’s also important to review the plan periodically to make sure it is still on track and to adjust it as needed. As I mentioned earlier, flexibility can be part of your plan.

Define Your Mission and Vision

Creating a mission and vision statement is an essential step when formulating a business plan. This simple exercise helps provide the necessary focus for the future of the business. It grounds the startup plan in its core values and overall purpose, allowing it to launch in an informed way with goals and expectations defined from the outset.

A company description should also be included as part of the mission and vision statement, so entrepreneurs will also need to consider how they want to market themselves to their customers or potential investors. They should ask questions such as: What are my company’s values? What products or services do I offer? How am I different from my competition? What are my short-term and long-term objectives?

Answering these questions early on will make crafting a cohesive mission statement much easier. After all, that statement needs to encompass everything that makes this particular business unique and successful.

SWOT Analysis to Structure Your Business Plan

The SWOT analysis is a great tool to help structure and develop an effective business plan. By conducting a Strengths, Weaknesses, Opportunities, and Threats (SWOT) analysis, you can gain insight into the overall competitive landscape of your current business position and determine which organizational strategies may be most effective for success.

This exercise can help solidify your competitive advantage in marketplaces with similar offerings. Moreover, doing a SWOT analysis can reveal areas of improvement where weaknesses could inhibit potential growth if not corrected or improved upon prior to proceeding with a business plan, such as customer service delays or product quality gaps.

A complete evaluation of the external environment should assess what current opportunities and threats may disrupt or enhance market presence. These considerations include factors such as changes in laws/regulations and economic landscapes because these are usually major determinants for company successes or failures.

Set Your Business Goals

I’ve already told you the first step for this part of the plan. You need your mission and vision clearly stated. In turn, the goals should speak to exactly how specific objectives will be implemented in order to reach these higher-level aspirations.

Will growth be measured by gross revenue? Profit? Personnel? Another metric such as physical office space? Whatever it may be, you should have a clear idea of how much growth you want to achieve annually—whether this is more customers, increased profit margins, or improved staff satisfaction. By defining measurable key performance indicators that align with your mission statement and business strategy, businesses can stay on track and measure progress along the way.

Determine Your Format

Creating a business plan format is an important step when launching any venture. For example, if starting a conventional business, the traditional approach of writing a comprehensive business plan should be undertaken.

This includes researching and analyzing markets, industry trends, and competitors, as well as creating an operational and financial roadmap for the organization. It should include market research to assess a target audience and outline strategies for product/service positioning, marketing efforts, and pricing schemes.

On the other hand, those wanting to launch in a more lean and agile way are able to start off with what's called a lean startup plan (more on that later.) This method lets founders focus on getting out of the building and talking to potential customers while minimizing risks associated with larger investments in terms of time or money upfront.

Ultimately selecting the right format depends upon the kind of company you’re trying to build or how much capital you’re willing to invest first into your project.

Traditional Business Plan

A traditional business plan is a document that outlines all the necessary components of a sound business strategy. It contains all the basics of setting up and operating a successful venture, including product and/or market research, target audience identification, capital requirements, marketing approach, organizational structure, staffing needs, management team backgrounds and experience. Writing a comprehensive and detailed traditional business plan takes more time than simpler plans, such as a lean plan or elevator pitch.

Lean Startup Plan

A lean startup plan is a key part of any new venture. It serves as the blueprint and roadmap for a company, providing insight into what needs to be done in order to become successful. For a plan to be considered “lean”, it typically follows a few key principles: focusing on the big picture, delivering as much as possible with minimal resources, and only involving stakeholders or partners when absolutely necessary.

Team Management Summary

This step is only for anybody who has a team!

Having an effective team is essential in any successful endeavor, and an effective team management summary can be the difference between success and failure. A team management summary outlines the roles, responsibilities, and time frames for tasks of each individual on your team. It’s important to establish clear expectations upfront so that everyone understands their role. (This is especially crucial for larger teams with many members.)

The summary should include a table detailing the various roles, responsibilities, and timelines specific to each member's task. For example, if there are three members on the team and their tasks are to develop a new app for a client, one may be responsible for coding and debugging, another may oversee the marketing of the app, and a third may do research into suitable technologies used in the app.

Each member should have specific timelines in this breakdown of tasks outlined in how long it will take them to complete their section, ensuring the timely completion of goals set. Ultimately, having an effective management summary can help ensure your team runs optimally while helping you keep track of progress toward your goal.

Define Your Target Client

Defining your target client and understanding their story is essential to succeeding in the real estate industry. Knowing who your ideal customer is, where they shop, what they want, and why they are interested in buying or renting a home gives you an advantage over other agents who just list properties without any knowledge of the actual customer.

When figuring out your target client's story, it's important to get as specific as possible. Ask questions that will give you insights into what they want and need in their current situation—from first-time homebuyers to retired couples looking for a place to retire or investors searching for short-term rentals.

Understanding your target customer inside and out allows you to better serve them by providing personalized advice and guidance on their journey toward finding their perfect home or investment property. With this in-depth knowledge of your customer's needs and preferences, you can come up with well-rounded strategies that successfully appeal to them.

Outline SMART Business Goals

In order to ensure that your real estate business goals are productive and attainable, the acronym SMART is a great way of tracking progress and holding yourself accountable for your goals. The SMART system stands for Specific, Measurable, Attainable, Realistic, and Timely which is essential when coming up with action plans in order to be successful.

To begin, focus on the goal you want to achieve and from there work backward by outlining specific objectives that have time frames attached. Each objective should also correspond to something measurable so it’s easier to evaluate results.

For example, if you want to increase qualified-lead generation by 20% each month using online resources such as social media, paid advertising and your company website then break it down into individual tasks such as creating ads on social media platforms or creating content for the website in order to drive more traffic.

With this method, instead of having an ambiguous goal, you know exactly how you plan on accomplishing it and can track your work accordingly. By setting SMART business goals, it allows us to not only reach our targets but to understand why we weren’t able to reach them when plans go astray so changes can be made in order for success going forward.

Develop a Marketing Plan

The creation of a marketing plan is important in any business because it helps to ensure that the organization's products and services reach the target audience, generate sufficient profits, and yield desired outcomes. When creating a marketing plan, there are four key elements to consider: product, price, place, and promotion.

You first need to understand what it is that your organization offers or sells and evaluate how differentiated your offering is from your competitors'. Second, careful consideration must be given to the pricing of said offer, ensuring that your prices are competitive yet still useful for generating a profit for the business.

Furthermore, particular attention should be paid to the benefits that customers will receive from doing business with you at this price point, making sure they are worth the investment. Once these core elements of product and pricing have been addressed, you can then move on to consider where and how you will promote your services. Which mediums will you utilize? Will you create ad campaigns online or through traditional channels? Considerations such as these form an integral part of developing an effective marketing strategy for any business.

Create a Financial Plan

Creating a financial plan is a critical step in writing your business plan. This section should cover both expenses and income to provide an overview of how the business functions. All expected business costs like overhead, fees, staffing, and materials must be accounted for as well as personal expenses that may arise due to the operation of the business.

Licensing should be considered when looking at expenses—ongoing education, running a business in multiple states, or even other changes that might come up through ownership. Attending conferences and trade shows may also need to be factored into the plan to help promote or increase the visibility of the products or services and reach potential customers.

It's a good idea to consider how your personal lifestyle will change due to your venture. There is something to be said about “dressing for success.” Soo … this could include items such as clothes for professional events or networking functions, as well as increased transportation costs for commuting to work or client meetings.

With all this taken into consideration, you can confidently move forward with your financial plan and come closer to making your dream of owning a successful business a reality.

Reach Out!

I’ve just given you the reasons why you need a business plan and told you what you need to do to create one. You have all the information you need to make it happen. Now you have some decisions to make and some tasks to accomplish.

Given all of that, if you still have questions or feel uncertain, reach out! You may benefit from a great mentor. I would love to be a resource for you.

The real estate business is always evolving, so finding a mentor and subscribing to as many blogs and mailing lists (like this one) are fundamental to your understanding of what it takes for you to succeed as a real estate agent.

So reach out, and let’s chat. I’d love to help you develop an amazing business plan and move your business from so-so to so-fantastic.